EUROTUNNEL 2003 PRELIMINARY RESULTS

Market leadership strengthened in a tough year

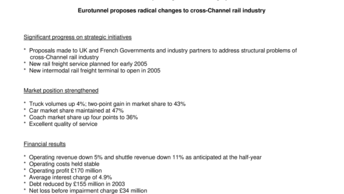

Eurotunnel proposes radical changes to cross-Channel rail industry

Significant progress on strategic initiatives

- Proposals made to UK and French Governments and industry partners to address structural problems of cross-Channel rail industry

- New rail freight service planned for early 2005

- New intermodal rail freight terminal to open in 2005

Market position strengthened

- Truck volumes up 4%; two-point gain in market share to 43%

- Car market share maintained at 47%

- Coach market share up four points to 36%

- Excellent quality of service

Financial results

- Operating revenue down 5% and shuttle revenue down 11% as anticipated at the half-year

- Operating costs held stable

- Operating profit £170 million

- Average interest charge of 4.9%

- Debt reduced by £155 million in 2003

- Net loss before impairment charge £34 million

- Impairment charge of £1.3 billion

Eurotunnel, operator of the Channel Tunnel, today announced its preliminary results for the year-ended 31 December 2003.

Richard Shirrefs, Chief Executive, said:

"2003 was a tough year with poor market conditions and intense price competition. Our excellent service quality enabled us to strengthen our market share, whilst a constant focus on improving efficiencies in the business enabled us to hold our costs stable. We are also pleased to see the recent improvement in passenger numbers from Eurostar. We reduced our debt by a further £155 million, bringing the total debt reduction since the 1998 financial restructuring to £1.2 billion.

"This time last year we said that Governments, the Railways and Eurotunnel needed to work together to increase traffic. To achieve this, the structural problems of the cross-Channel rail industry, including under-utilisation of expensive infrastructure, financial losses of all the operators, and conflicting contractual relationships, need to be addressed.

"We have made proposals to the UK and French Governments and our industry partners which seek to stimulate growth in rail passenger and rail freight volumes, improve our profitability, and get our financing onto a sensible and sustainable basis once and for all."

Turnover

Operating revenue fell by 5% to £566 million. Revenue from Shuttle Services fell by 11% to £309 million at constant exchange rates, principally due to the impact of lower average yields from the truck and car businesses, which offset increased carryings in the truck business. Railways revenue increased slightly to £232 million as a result of inflation, and remains protected until November 2006 by Minimum Usage Charge payments under the Rail Usage Contract.

Revenue of £25 million was generated from non-transport activities in 2003, including retail and telecoms revenues, and proceeds of £7 million from the sale of land in the UK.

Other income of £18 million largely comprised the release of provisions for large-scale maintenance. The increase in this non-cash item offsets increased operating costs during 2003 relating to the mid-life refit of the Shuttle fleet.

Operating profit

The operating profit of £170 million was down 18%. Operating costs were stable at £ 259 million, with increases in insurance premiums and maintenance costs relating to the mid-life refit of the Shuttle fleet offset by cost reductions including lower energy costs. The increase in cost of sales reflects the value of land stocks disposed of during the year.

At £146 million, depreciation and provisions increased by £5 million compared to 2002 as a result of higher Tunnel depreciation charges.

Net result

The net result before impairment charge was a loss of £34 million.

Net interest costs in 2003 were £318 million, reflecting an average interest rate of 4.9%. The increase compared to 2002 reflects a £17 million non-recurring reduction to 2002 interest charges as a result of financial operations concluded during that year. The reduction in 2003 interest charges resulting from debt repurchases, contributed to an underlying improvement of £10 million in the interest charge for 2003 compared to 2002.

The exceptional profit of £115 million comprised the profit arising from three UK leasing company acquisitions, and the profit generated from the repurchase of debt at a substantial discount to face value with the cash proceeds of such transactions.

The valuation of the Group's assets has been carried out in accordance with IAS36 (equivalent to FRS11) which compares the net book value of assets with the discounted future value of cash flows. The result of this valuation is an impairment charge of £1.3 billion. The application of this standard at 31 December 2003 gives rise to a value in use £1.3 billion lower than the net book value of assets. This impairment charge reflects lower projected cash flows in the light of the 2003 results and the consequences of these lower projected cash flows on the sustainable level of debt, together with higher market interest rates.

The impairment charge recorded in the accounts reduces shareholders funds and will reduce the future depreciation charge by approximately £17 million per annum. This impairment charge has no impact on the Group's liquidity position or its loan covenants. The net loss for the year after the impairment charge was £1,334 million.

Cash flow and interest cover

Cash flow from operating activities was £315 million in 2003. The majority of the reduction compared to 2002 was due to lower Shuttle revenues, with the balance accounted for by exchange rate and working capital movements.

Net capital expenditure fell from £41 million in 2002 to £25 million in 2003, resulting in net cash flow from operating activities after capital expenditure of £290 million.

Interest cover after capital expenditure (which measures cash flow after capital expenditure as a proportion of the net interest charge due) was 90%. This compares with the 2002 result of 102%, which included a non-recurring benefit of £17 million from financial operations.

Financial operations

Eurotunnel's £6.4 billion debt carries an average interest rate of 4.9%. No debt repayments are due before 2006.

During 2003, three UK leasing companies were acquired, generating £25 million in cash. With this cash, together with the cash generated from similar transactions in 2002, Eurotunnel repurchased or repaid £155 million of debt. Interest charges were reduced by £5 million.

Strategic developments

Radical restructuring of the cross-Channel rail industry

Eurotunnel has made proposals to the UK and French Governments and its industry partners which seek to address the structural problems faced by the cross-Channel rail industry. These proposals are set out in a separate press release.

Rail freight traction service

Eurotunnel's request for an operator's licence in France is being considered by the French Transport Ministry and a decision is expected imminently. Starting in early 2005, Eurotunnel will haul trains between Bâle and Dollands Moor on a rail freight corridor linking Milan (Italy), Bâle (Switzerland), Metz (France, for connections to Germany and Eastern Europe), Dourges (France), and the Midlands. There is already significant interest from potential customers.

The service is expected to comprise five trains per week in each direction on this route from 2005, increasing to 30 trains per week in each direction by 2008.

The introduction of this new rail freight service via the Channel Tunnel will reduce journey times by up to one day compared to shipment across the North Sea, and have significant environmental benefits by shifting freight from road to rail. Eurotunnel is actively exploring other rail freight route opportunities.

Rail freight terminal

Eurotunnel has commenced work on an intermodal rail freight terminal, allowing continental gauge trains to access UK markets for the first time. FIRST (Folkestone International Rail Freight Services Terminal), which is expected to open in mid- 2005, will be built alongside Eurotunnel’s existing tracks on its Folkestone site. This will provide the only access to UK markets for larger continental rail vehicles.

The intermodal terminal will initially be able to handle up to four trains per day in each direction. It will be equipped to handle ‘piggyback’ trailers, high-cube swapbodies and containers on conventional flat wagons.

If traffic from these two initial projects develops as currently expected the net contribution would be around £13 million per annum, almost doubling the contribution compared to today's rail freight traffic levels. However, these services are also designed to stimulate interest in cross-Channel rail freight and encourage other operators to develop services. This would further increase the overall contribution of rail freight.

Concluding, Charles Mackay, Chairman of the Joint Board, said:

"Although commentators are increasingly more optimistic about the overall economic prospects for 2004, there are still no signs of improvement in the cross-Channel market. The market remains depressed and price competition is fierce. At this point it is therefore difficult to predict when our shuttle business will pick up again.

"We have put forward proposals to address the current structural problems of the cross-Channel rail industry. It took courage, imagination and real political will to build the Channel Tunnel. We need a little more of each to finally get the most out of one of the great engineering triumphs of the 20th century."

Notes to editors:

- The message to shareholders from the Chairman of the Joint Board and the Chief Executive is attached.

- The summary Eurotunnel Group Combined Accounts and the financial analysis are attached.

- A conference call for UK news wires will be held at 0730 (UK time) today. Tel: + 44 (0) 20 7784 1017. A replayof the call will be available on tel: + 44 (0) 20 7784 1024 (Code: 487653).

- A conference call for UK/US analysts will be held at 1300 (UK time) today. From the UK tel: + 44 (0) 20 7784 1017. From the US tel: + 1 718 354 1158. A replay of the call will be available from the UK on + 44 (0) 20 7784 1024, and from the US on + 1 718 354 1112 (Code: 334366).

- An interview with Richard Shirrefs, Chief Executive, in video/audio and text format will be available from 0800 (UK time) today on www.eurotunnel.com.

Get the full results in the attached document below.

Strategy unfolding

A difficult environment

Having made good progress until 2002, the Group was hard hit in 2003 by the economic climate and the international political situation, which were particularly unfavourable to the tourism and transport sectors. The ferries, faced with a depressed market and excess capacity, adopted a pricing policy that impacted on average market yields and therefore on the income generated by our primary shuttle business. This more than cancelled out the increased volumes on our truck shuttle service.

In spite of this difficult environment, the outstanding quality of our services enabled us to strengthen our position in the market. The sustained effort we have put into increasing productivity allowed us to hold operating costs stable. We were therefore able to limit the reduction in operating profit to 18%, which at £170 million is still at a very profitable 30% of our operating revenues of £566 million (down 5%).

The net loss before impairment charge is limited to £34 million thanks to an exceptional profit of £115 million from financial operations. We have recorded an impairment charge of £1 300 million as explained in the financial analysis. This impairment charge does not impact on the Group’s cash position or loan agreements, and reduces the annual depreciation charge by approximately £17 million from 2004.

During the year, we reduced our debt by a further £155 million, bringing the total reduction of debt since the financial restructuring of 1998 to £1.2 billion. The average interest rate, at 4.9%, is very low and no loans fall due before 2006.

Although commentators are increasingly more optimistic about the overall economic prospects for 2004, there are still no signs of improvement in the cross-Channel market. The market remains depressed and price competition is fierce. At this point it is therefore difficult to predict when our shuttle business will pick up again.

Strategic progress

At the last Annual General Meetings, we presented three new strategic directions for the next few years to reinforce the existing strategy of developing shuttle revenues, controlling costs and reducing debt. The new strategic initiatives focused on becoming a driving force for rail freight development, acting as a dynamic partner in regional development, and instigating proposals to restructure the cross-Channel rail industry.

We made considerable progress in all three areas in 2003.

As far as rail freight is concerned, our operator’s licence will enable us to launch a new cross-Channel service. From early 2005, Eurotunnel will be able to run trains between Basle in Switzerland and Dollands Moor near Ashford in Kent. This is the key sector of the freight corridor linking Milan, Basle, Metz (for connections to Germany and Eastern Europe), Dourges (near Lille) and the industrial and commercial centres of the United Kingdom. Several potential customers have already shown their interest in this service.

In addition, we are starting construction of an intermodal freight platform at our Folkestone terminal, which will for the first time allow standard Continental gauge goods trains to access the British market. This new terminal should be operational by 2005; this will then be the only point of entry to the United Kingdom for Continental wagons of this gauge.

If the traffic resulting from these two projects develops as we envisage, we can expect the contribution of our rail freight business to double. Moreover, these new services should spark off interest in cross-Channel rail freight and encourage other operators to use the Tunnel.

As an active partner in regional development, we are working with local authorities to promote and implement all the economic, cultural and tourist-related initiatives that are likely to increase the attractiveness of Kent and the Nord-Pas de Calais and therefore, in the long term, increase use of the Tunnel.

Finally, the most important part of our strategy consists in finding solutions to the structural problems facing the cross-Channel rail industry, and Eurotunnel announced today its Galaxie Project.

Galaxie Project

Eurotunnel has made proposals to the UK and French Governments and its industry partners which seek to address the structural problems faced by the cross-Channel rail industry.

The cross-Channel rail industry currently suffers from under-utilisation of expensive infrastructure, financial losses and conflicting contractual relationships. In particular the high level of access charges paid by rail companies for the use of the Channel Tunnel is holding back traffic growth. Eurotunnel’s current financial structure leaves it with no scope to reduce these charges unilaterally.

Eurotunnel has conducted a detailed analysis of the industry for over a year in order to identify solutions for the complex issues underlying the industry’s difficulties. The key elements of any solution must include the alignment of the interests of the cross-Channel operators and clear incentives to increase traffic through the Tunnel, within a stable financial structure.

Eurotunnel is proposing to significantly reduce access rates for train operators in a manner which will align the incentives of the cross-Channel operators and reduce their costs. This should enable Eurostar to increase its traffic to existing destinations and would assist the introduction of new destinations such as Amsterdam. Lower Tunnel access rates will also considerably increase the size of the economically viable cross-Channel rail freight market. The reduced access rates should therefore be partly compensated for by increased traffic.

To achieve these access charge reductions, Eurotunnel requires a more stable financial structure, which would involve a significant reduction in the amount of its debt and interest payments, as well as an extension of debt maturities. Eurotunnel and its advisers have developed a series of detailed proposals to meet these objectives. Eurotunnel now expects constructive engagement with its industrial and financial partners.

Eurotunnel is seeking to reach agreement in principle during 2004 with implementation in 2005. However, the issues are complex and there can be no assurance as to the eventual outcome at this stage.

* * * * *

Ten years after the opening of the Tunnel, it is clear that our structural problems, which are due to the strictly private-sector funding of the project, an excessively high debt level and insufficient rail traffic, cannot easily be resolved without a comprehensive and innovative approach to the problems faced by all the stakeholders of the cross-Channel rail industry.

The Galaxie project gives our shareholders realistic hope of seeing Eurotunnel emerge from its financial difficulties once and for all. By contrast, the unrealistic and often mutually contradictory ideas put forward by certain dissident shareholders do not represent a strategic solution for the future of the company and carry a serious risk that shareholders lose all the value of their investment.

Getting the Tunnel built required courage, imagination and real political will. Today, we need a little more of each of these, plus the support of all concerned – our shareholders and employees, our industrial partners and the authorities - to turn the greatest civil engineering project of the 20th century into a profitable investment.

Charles Mackay

Chairman of the Joint Board

Richard Shirrefs

Chief Executive