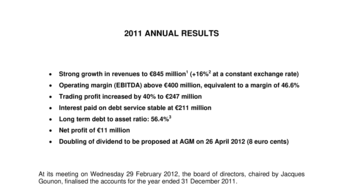

2011 ANNUAL RESULTS

Strong growth in revenues to €845 million1 (+16%2 at a constant exchange rate) Operating margin (EBITDA) above €400 million, equivalent to a margin of 46.6% Trading profit increased by 40% to €247 million

Interest paid on debt service stable at €211 million

Long term debt to asset ratio: 56.4%3 Net profit of €11 million

Doubling of dividend to be proposed at AGM on 26 April 2012 (8 euro cents

At its meeting on Wednesday 29 February 2012, the board of directors, chaired by Jacques Gounon, finalised the accounts for the year ended 31 December 2011.

Jacques Gounon, Chairman and Chief Executive Officer of Groupe Eurotunnel SA, stated:

“In 2011, the Eurotunnel Group made a clear profit and generated significant cash flows despite the uncertain economic climate. The outlook is positive and, as a sign of our confidence in the future, we will ask the shareholders to vote at the AGM for the doubling of the dividend to €0.08 for the 2011 financial year.”

IMPORTANT EVENTS IN THE PAST YEAR

- Dynamic cash flow management

Eurotunnel continues to generate a significant operating cash flow.

- Added value for shareholders

Following the conversion of the 2007 Warrants4 which enabled shareholders to benefit from the increase in value achieved within the Eurotunnel Group and the various transactions to simplify its financial structure, Groupe Eurotunnel SA has a capital composed of 561 million shares compared to maximum of 613 million projected in 2007. Since the financial restructuring in 2007 and following the final exercise of the 2007 Warrants the combined effect of the transactions completed has led to an increase in value of almost 9%.

- Purchase of €147 million5 of floating rate notes

Groupe Eurotunnel SA has taken advantage of its significant cash reserves to optimise the management of its debt, by buying €147 million of discounted notes. This represents a full-year reduction in interest charges estimated at €5 million in 2012. The nominal value of the long term debt less the floating rate notes is €3.6 billion. The long term debt to asset ratio is 56.4%.

- The cross-Channel Fixed Link

In 2011 almost 19 million people and approximately 17.7 million tonnes of freight crossed the Channel using the Tunnel.

Sustained growth in Passenger and Truck Shuttle activity.

Eurotunnel won the IFW Environment Award, for Leadership in Sustainable

Development at the awards ceremony organised by International Freighting Weekly, Europe’s leading transport and logistics publication.

2% increase in the number of Eurostar passengers to nearly 9.7 million in 2011.

Commissioning of four SAFE stations (fire suppression zones), a major innovation to further strengthen the safety of the Channel Tunnel.

- Europorte

GB Railfreight, the UK subsidiary of Europorte and third largest rail freight operator in the UK, won the top prize for Freight and Logistics at Rail Magazine’s National Rail Awards 2011.

A positive contribution to 2011 revenues (€158 million). Europorte’s offer is based on punctuality and quality of service, which ensured the continuation of all existing contracts for Europorte France and the signing of new contracts, notably with leading European transport and logistics operator GEFCO.

Acquisition of 28 locomotives, notably the Vossloh Euro 4000 diesel-electrics, currently the most powerful in Europe.

The recruitment of c.100 drivers in France as part of the strategy to develop sustainable freight transport and to generate skilled jobs.

- CIFFCO (Centre International de Formation Ferroviaire de la Côte d’Opale)6

Creation of the first private training centre specialising in railway skills

This is the first time that a privately owned transport group has created such a training centre, open to all European railway and infrastructure maintenance companies and their subcontractors, as well as those from neighbouring countries. CIFFCO is accredited by the French Public Safety authority (EPSF) and delivers courses for fifteen different skills. It is able to provide training for technicians working on the French national network as well as those of neighbouring countries.

FINANCIAL RESULTS

At €403 million, the operating margin (EBITDA) increased compared to 2010 as a result of good cost control and the trading profit increased by €70 million to €247 million in 2011 (+40%)7.

Operating profit (EBIT) also increased, by €85 million, including insurance indemnities totalling €29 million relating to the fire in September 2008.

In 2011, the available cash flow enabled the payment of a dividend (€21 million), the purchase of variable rate notes issued by Channel Link Enterprises Finance (CLEF, the debt securitisation structure), for €128 million, the purchase of own shares (€40 million) and capital expenditure of €98 million. At 31 December 2011, cash and cash equivalents amounted to €276 million.

OUTLOOK

The Queen’s Jubilee in June 2012: bookings taken for this long weekend are already on the increase. The number of booths available will be more than doubled to ease passport controls and improve speed and traffic flow, always an objective of the business.

London 2012 Olympic Games: the Eurotunnel Group is preparing itself to manage the waves of passengers and will speed up Shuttle crossing times to just 30 minutes, instead of the normal 35 minutes. Shuttle speed will be increased to 100 mph compared to 90 mph today.

The upturn in activity appears to be continuing, but will remain gradual according to the segment. In the medium term, the Group remains confident in its ability to generate sustainable growth and, through the development of its different vectors for growth, to improve its resistance and responsiveness to the vagaries of the economy.

Eurotunnel maintains its interest in the purchase of the three ex-Seafrance ferries. The Group is organising the resources necessary to develop this new activity in line with its criteria for profitability and for the benefit of the Nord-Pas-de-Calais region.

Get the full results in the attached document

- The figures for the Group’s consolidated income statement in 2010 have been recalculated at the average exchange rate for 2011 (£1=€1.148), to enable a better comparison between the two periods.

- Like for like, taking account of the GB Railfreight revenues for the period from January to May 2010 (before its acquisition by the Eurotunnel Group on 28 May 2010), the growth in the Group’s consolidated revenue is 11%.

- The Group defines its long term debt to asset ratio as the ratio between long-term financial liabilities less the value of the floating rate notes which were purchased during 2011 as a percentage of tangible fixed assets. At 31 December 2010 the ratio was 56.1%. The calculation of this ratio is set out in section 4 below.

- Warrants for shares issued in 2007: securities note approved by the Autorité des marches financiers (AMF) on 4 April 2007 (visa n° 07-113) and delisted from the NYSE Euronext Paris market before opening on 2 January 2012.

-

Calculated at the exchange rate at 31 December 2011 of £1=€1.197.

-

The Opal Coast International Railway Training School

- Includes insurance indemnities of €9 million relating to the operating losses following the fire in September 2008